Climate‑Related Financial Disclosures (ASRS)

Service Overview

We provide end-to-end climate-related financial disclosure services aligned with the Australian Sustainability Reporting Standards (ASRS), including AASB S2. Support spans preparation, implementation and reporting, helping organisations meet compliance requirements, strengthen governance and support long-term value creation.

Typical Activities

- AASB S2 preparation

- AASB S2 implementation

- AASB S2 reporting

We provide end-to-end climate-related financial disclosure services aligned with the Australian Sustainability Reporting Standards (ASRS), including AASB S2. Support spans preparation, implementation and reporting, helping organisations meet compliance requirements, strengthen governance and support long-term value creation.

Understanding AASB S2 Requirements

AASBS2 details climate-related financial disclosure requirements under the Australian Sustainability Reporting Standards. The standard applies to both listed and private organisations that meet specified size, revenue or emissions thresholds.

Aligned with international reporting frameworks, including the ISSB Standards, AASB S2 requires organisations to assess and disclose the financial impacts of climate-related risks and opportunities. The standard requires disclosures across governance, strategy, risk management, and metrics and targets, helping organisations communicate the potential financial impacts of climate-related risks and opportunities.

Australia's mandatory climate-related financial reporting requirements are being introduced through a phased approach. The first reporting entities covered financial years commencing from 1 January 2025, and additional organisations are coming into scope in subsequent years. Early preparation helps organisations understand reporting obligations, establish appropriate governance arrangements, and develop the processes and systems needed to support reliable climate-related disclosures.

.avif)

Key AASB S2 Disclosure Requirements

AASB S2 is structured around four core pillars:

- Governance: How climate-related risks and opportunities are overseen and managed across the organisation.

- Strategy: How climate-related risks and opportunities may affect the organisation's strategy, operations and financial performance.

- Risk Management: The processes used to identify, assess and respond to climate-related risks and opportunities.

- Metrics and Targets: The measures used to monitor performance and track progress against climate-related objectives.

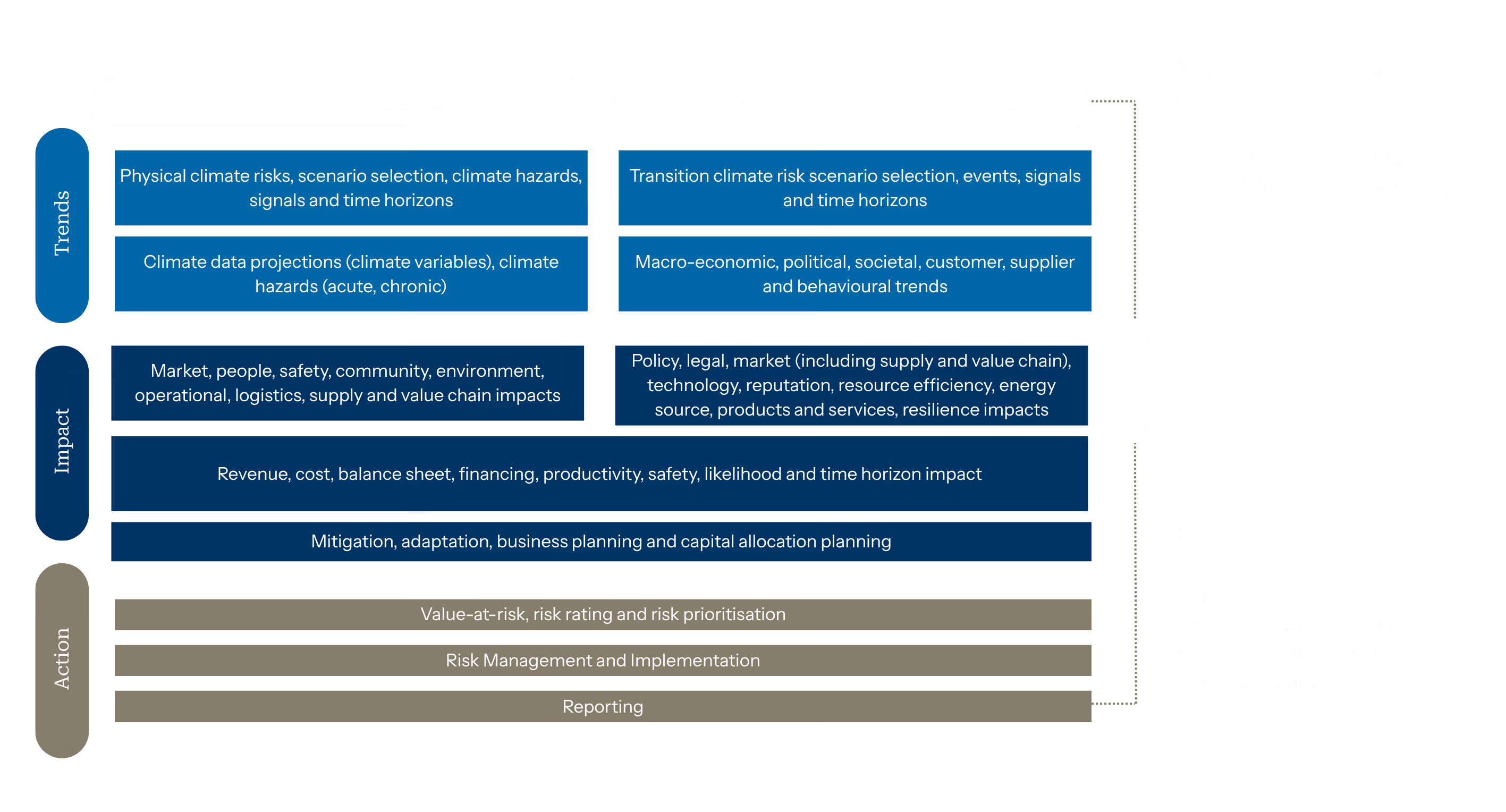

Central to these requirements is understanding how climate-related risks and opportunities (CRROs) may affect an organisation and how they are identified, assessed and managed.

Our Approach to AASB S2

We encourage organisations with reporting obligations to begin preparing as early as possible and build capability progressively across three stages.

Building Readiness for AASB S2

The first stage is understanding your organisation's current position. We support gap assessments and action prioritisation, translating AASB S2 requirements into a practical roadmap aligned with organisational structures, resources and reporting timeframes. This includes assessing existing governance arrangements, risk management processes, climate-related risks and opportunities, and metrics and targets.

Identifying Climate-Related Risks and Opportunities

The second stage focuses on identifying and assessing climate-related risks and opportunities (CRROs). This is often one of the most complex aspects of AASB S2 implementation. We help organisations assess exposures, understand potential impacts and integrate findings into strategy, risk management and business planning processes.

For quantitative scenario analysis, we use a combination of CMIP5 and CMIP6 climate models to assess future climate conditions at regional, sub-regional and local scales. Climate projections are complemented by macroeconomic scenarios from the Network for Greening the Financial System (NGFS) and the International Energy Agency (IEA), alongside local market and policy insights.

Climate Reporting and Assurance Readiness

The final stage focuses on preparing climate-related disclosures and establishing reporting processes. This includes strawman and iterative report development, disclosure drafting, report preparation and pre-audit climate disclosure reviews to support clear, consistent and assurance-ready reporting. While we can support assurance readiness, formal assurance must be undertaken by your external auditor.

Supporting Ongoing Climate Disclosure and Governance

Meeting AASB S2 requirements involves more than a one-off reporting exercise. We help organisations embed the governance, processes and controls needed to support the ongoing management and disclosure of climate-related risks and opportunities. This includes strengthening governance arrangements, improving data quality and preparing clear, consistent and assurance-ready disclosures.

SISAH has embraced mandatory climate reporting as an opportunity to lead the industry by strengthening governance and committing to credible decarbonisation. Partnering with Pangolin Associates gave us expert guidance across 10+ subsidiaries, from gap analysis to harmonised workstreams and audit-ready disclosures. Their clear, collaborative approach ensured compliance while building the foundation for SISAH’s long-term climate resilience and leadership.

Don Burnett

Don Burnett - Chief Financial Officer at SISAH

Request a call back

We welcome your enquiries about sustainability and carbon management.

Follow us on LinkedIn

Industry Expertise, Shaped by Real-World Experience